All Categories

Featured

Table of Contents

The main distinctions in between a term life insurance coverage policy and a permanent insurance plan (such as entire life or universal life insurance policy) are the period of the plan, the buildup of a cash money worth, and the cost. The right choice for you will certainly depend on your demands. Here are some things to think about.

Individuals who own entire life insurance policy pay more in costs for much less coverage yet have the safety of understanding they are protected permanently. Term life insurance with fixed premiums. People that acquire term life pay premiums for an extended period, however they obtain absolutely nothing in return unless they have the bad luck to die before the term ends

The efficiency of long-term insurance coverage can be stable and it is tax-advantaged, offering additional benefits when the supply market is unpredictable. There is no one-size-fits-all response to the term versus irreversible insurance coverage discussion.

The biker ensures the right to transform an in-force term policyor one ready to expireto a permanent plan without undergoing underwriting or verifying insurability. The conversion biker must enable you to convert to any type of permanent policy the insurance policy company uses with no constraints. The main attributes of the rider are preserving the initial health score of the term policy upon conversion (also if you later on have health issues or become uninsurable) and choosing when and how much of the coverage to convert.

Why is Level Term Life Insurance Vs Whole Life important?

Of program, general costs will certainly raise significantly since entire life insurance policy is much more pricey than term life insurance. The benefit is the ensured approval without a medical exam. Clinical problems that create throughout the term life period can not trigger premiums to be enhanced. The firm might require restricted or full underwriting if you want to include added cyclists to the new policy, such as a lasting care motorcyclist.

Term life insurance is a reasonably economical method to offer a round figure to your dependents if something happens to you. If you are young and healthy, and you support a family, it can be a great choice. Whole life insurance policy features significantly greater regular monthly premiums. It is meant to give insurance coverage for as lengthy as you live.

It depends on their age. Insurance policy firms established an optimum age limitation for term life insurance coverage policies. This is normally 80 to 90 years of ages, but may be greater or lower depending on the business. The premium additionally increases with age, so an individual aged 60 or 70 will certainly pay considerably greater than a person years younger.

Term life is rather similar to automobile insurance. It's statistically not likely that you'll need it, and the premiums are cash down the tubes if you do not. If the worst happens, your household will get the advantages.

What should I look for in a Term Life Insurance With Fixed Premiums plan?

___ Aon Insurance Solutions is the brand name for the broker agent and program management operations of Affinity Insurance coverage Services, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Fondness Insurance Firm, Inc. (CA 0795465); in Alright, AIS Fondness Insurance Policy Services Inc.; in CA, Aon Fondness Insurance Coverage Providers, Inc.

The Plan Representative of the AICPA Insurance Trust, Aon Insurance Providers, is not associated with Prudential. Group Insurance protection is provided by The Prudential Insurance Policy Company of America, a Prudential Financial firm, Newark, NJ.

Generally, there are two kinds of life insurance prepares - either term or permanent plans or some mix of both. Life insurance companies offer different forms of term strategies and typical life policies in addition to "interest delicate" products which have ended up being a lot more common because the 1980's.

Term insurance provides defense for a specified time period - Level term life insurance calculator. This period could be as short as one year or offer insurance coverage for a specific variety of years such as 5, 10, two decades or to a specified age such as 80 or in some instances as much as the oldest age in the life insurance coverage death tables

Is there a budget-friendly Level Term Life Insurance Vs Whole Life option?

Currently term insurance policy prices are really affordable and amongst the most affordable traditionally knowledgeable. It needs to be kept in mind that it is a widely held belief that term insurance is the least expensive pure life insurance policy coverage offered. One requires to review the plan terms very carefully to choose which term life choices appropriate to meet your particular circumstances.

With each brand-new term the premium is increased. The right to restore the plan without proof of insurability is an important advantage to you. Otherwise, the threat you take is that your health and wellness may weaken and you might be incapable to obtain a plan at the exact same prices or perhaps whatsoever, leaving you and your beneficiaries without insurance coverage.

You need to exercise this alternative during the conversion duration. The size of the conversion duration will certainly vary relying on the kind of term policy purchased. If you transform within the recommended duration, you are not needed to give any type of info about your health. The premium price you pay on conversion is normally based upon your "existing acquired age", which is your age on the conversion day.

How do I choose the right Level Term Life Insurance Calculator?

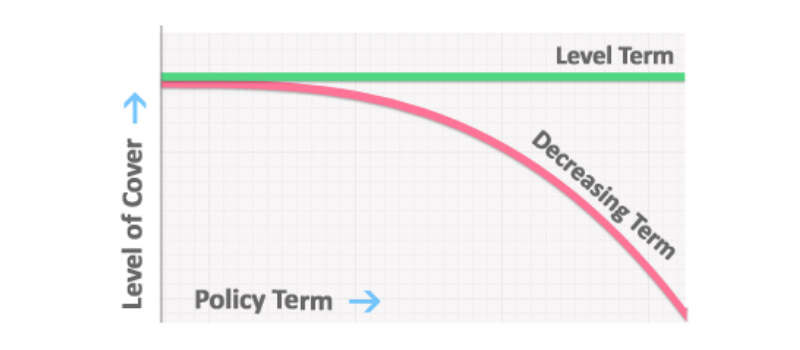

Under a degree term policy the face quantity of the plan stays the exact same for the entire duration. Typically such plans are sold as home loan protection with the amount of insurance lowering as the equilibrium of the home loan decreases.

Commonly, insurance firms have not can transform costs after the plan is marketed. Considering that such policies might proceed for years, insurance firms must make use of traditional mortality, rate of interest and expenditure price price quotes in the premium calculation. Adjustable premium insurance, however, enables insurance providers to provide insurance policy at lower "current" premiums based upon much less conservative assumptions with the right to change these premiums in the future.

While term insurance is created to supply protection for a defined amount of time, long-term insurance policy is designed to supply protection for your entire life time. To maintain the costs price level, the costs at the more youthful ages surpasses the actual expense of protection. This extra costs develops a book (money worth) which helps spend for the policy in later years as the expense of protection increases above the premium.

Level Term Life Insurance Calculator

With level term insurance coverage, the cost of the insurance policy will stay the exact same (or possibly reduce if dividends are paid) over the regard to your plan, normally 10 or twenty years. Unlike irreversible life insurance policy, which never ever expires as long as you pay costs, a level term life insurance coverage policy will finish eventually in the future, commonly at the end of the duration of your degree term.

As a result of this, lots of people use irreversible insurance coverage as a stable monetary preparation tool that can offer numerous needs. You might be able to transform some, or all, of your term insurance coverage throughout a set duration, generally the initial ten years of your plan, without requiring to re-qualify for coverage also if your health has actually changed.

How does Low Cost Level Term Life Insurance work?

As it does, you may desire to include to your insurance coverage in the future. As this occurs, you may want to at some point minimize your fatality advantage or think about converting your term insurance to a permanent plan.

Long as you pay your premiums, you can rest easy understanding that your enjoyed ones will get a death benefit if you pass away during the term. Numerous term plans allow you the capability to convert to long-term insurance policy without having to take one more health and wellness exam. This can allow you to benefit from the additional advantages of a long-term plan.

{kind=link}

Latest Posts

Aaa Burial Insurance

Best Final Expense Insurance Company To Work For

Final Expense Network Reviews